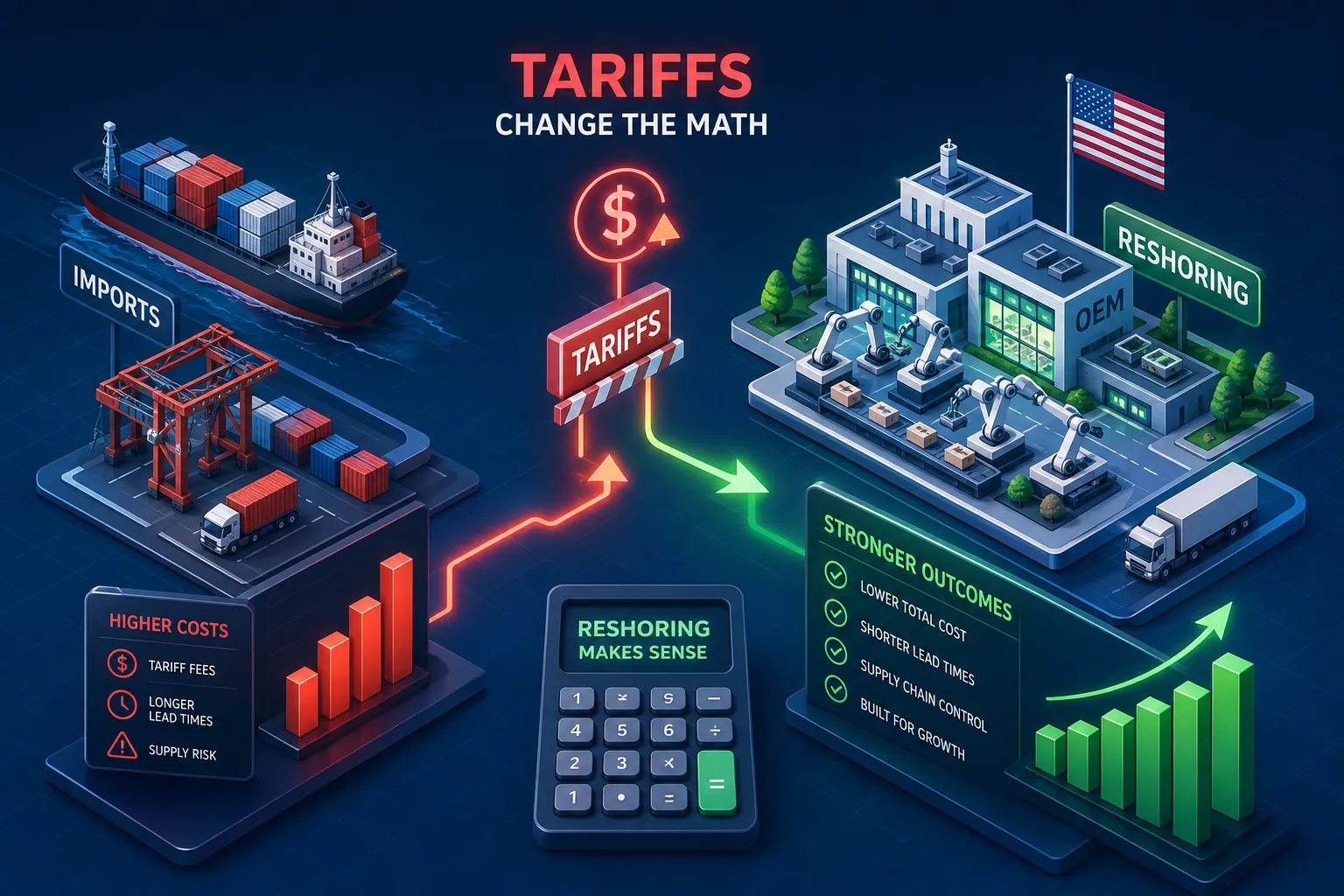

How do tariffs affect the decision to reshore electronics production from China? For most U.S. OEMs, the answer is already written in their landed cost models, they just haven’t updated those models yet. The cost assumptions that made Chinese electronics manufacturing look like the obvious choice were built in a different trade environment. For OEMs sourcing PCBs, passive components, and finished assemblies from China, the math that closed in 2020 no longer closes in 2026. Tariff stacking has quietly added 25 to 75 percentage points to the effective import rate across a wide range of electronics product categories, semiconductors and hybrid assemblies bearing the heaviest exposure, and Federal Reserve and NBER analyses of the 2025 tariff regime put the passthrough rate at 80 to 94 percent. Your Chinese supplier is not absorbing this. You are.

This article gives you the framework to run the numbers yourself. You’ll learn how the tariff layers combine, how to model total landed cost across three manufacturing geographies, and how to use the 2026 incentive environment to offset reshoring capital costs before the window closes. North American contract manufacturers have matured considerably in capability and automation investment. For many product programs, the cost-competitive case for domestic or nearshore production already exists. The landed cost analysis for electronics just has to happen.

Why the tariff stack hits electronics harder than most industries

The three tariff layers and how they combine

Most supply chain managers check one tariff rate and move on. The problem with electronics imports from China is that you’re not dealing with one tariff, you’re dealing with multiple layers that can apply simultaneously. Section 301 tariffs cover a broad range of electronics components at rates between 25 and 50 percent. A separate 25 percent tariff on semiconductors has been proposed under Section 232 authority, though applicability to specific HTS codes such as 8541 and 8542 should be verified against current USITC and Customs guidance before modeling. The universal reciprocal tariff applies a baseline 10 percent on most goods from China. For further context on how recent measures are affecting electronics manufacturers, see this analysis of China tariffs on electronics manufacturers.

When these layers stack, the effective rate compounds quickly. A semiconductor may face 50 percent under Section 301 plus an additional Section 232 levy, pushing the combined rate well past 60 percent before any universal rate is counted. A cost model that assumes a 25 percent duty on a semiconductor component classified under HTS 8541 or 8542 may be off by 30 percentage points or more depending on which measures apply. Verify your exact HTS classifications against current USITC rulings before finalizing any landed cost model, and consult an up-to-date tariff tracker when building scenarios.

How tariffs affect reshoring decisions across electronics categories

Effective tariff rates vary significantly by category as of mid-2026. Semiconductors run 50 to 75 percent; passive and active components, resistors, capacitors, logic devices, sit at 25 to 40 percent; rigid and flex PCBs fall in the 25 to 30 percent range; and hybrid assemblies such as displays, power supplies, and HMIs can reach 25 to 50 percent or higher when multiple classifications apply. Finished consumer electronics like smartphones and laptops currently hold a temporary exemption from the universal reciprocal tariff, but the White House has flagged this category for sector-specific measures. The word “temporary” deserves real weight in your planning horizon.

The passthrough reality OEMs need to accept

Federal Reserve and NBER analyses of the 2025 tariff regime put the passthrough rate at 80 to 94 percent. Chinese suppliers are not reducing prices to offset duties; they don’t have to, because U.S. importers have limited near-term alternatives for many components. This means the cost assumptions built into your 2022 or 2020 BOM analysis are materially wrong today. In many cases, pre-2025 models understate total landed cost by 30 to 50 percent once current effective tariff rates are applied at the component line-item level. Every landed cost model you’re using to evaluate program economics needs to be rebuilt. For a summary of academic findings on tariff pass-through, see the NBER digest on U.S. tariff pass-through.

How to calculate your real landed cost from China

The four components of a complete landed cost model

Total landed cost has four components, and most OEM cost models miss at least one of them. The first is bill of materials cost. The second is inbound logistics to the factory, the cost to get raw materials and components to your CM. The third is manufacturing and overhead, the “ex works” price. The fourth is outbound freight, duties, and insurance from factory to final destination. Each component behaves differently depending on geography, and duties are where the China model breaks hardest.

A worked example: a $50 BOM PCB assembly, China versus Mexico

Start with a $50 bill of materials for a representative PCB assembly. China-based manufacturing produces a finished unit at $68.18 on the factory floor, benefiting from lower overhead structures. After outbound ocean freight (5 percent of finished good value) and a 25 percent Section 301 tariff, that unit lands in the U.S. at $88.63. Mexico produces the same finished unit at $81.38 due to higher overhead structures, but outbound land freight runs just 2 percent of the finished good value, and USMCA eliminates the import duty entirely. That unit lands at $83.01.

The $13.20 per-unit production cost advantage China holds gets wiped out by tariffs and logistics, and then some. The China unit costs $5.62 more to land despite being $13.20 cheaper to build. At current Section 301 semiconductor rates of 50 percent or higher, the gap on component-heavy programs widens dramatically.

Where the China cost model breaks down

For this product example, the breakeven is already crossed at 25 percent Section 301 rates. You don’t need a dramatic tariff escalation for reshoring to pencil out, you’re already past the threshold for a significant portion of the electronics BOM. The programs most exposed are those with high semiconductor content, significant passive component counts, or hybrid assemblies that trigger multiple HTS classifications simultaneously. Identify those programs first.

China vs. Mexico vs. U.S.: what the three-location comparison actually shows

Why Mexico often wins on total landed cost despite higher production costs

Mexico’s hourly labor rate is actually lower than China’s, approximately $4.50 to $4.90 per hour versus $6.50 in China. Despite that labor advantage, Mexico’s overhead structure pushes the finished production cost roughly 19 percent higher per unit than China on the factory floor. That sounds like a disadvantage until you load in tariffs and freight. USMCA eliminates import duties entirely on qualifying electronics. Land freight transit runs 2 to 7 days, compared to 20 to 40 days by ocean. For mid-volume programs in the 100,000 to 2,000,000 annual unit range, nearshoring electronics from China to Mexico frequently delivers the lowest total landed cost of the three geographies; for more on logistics comparisons see this Mexico vs. China manufacturing: a logistics comparison.

When domestic U.S. production becomes cost-competitive

Domestic production carries the highest labor and overhead costs, but it eliminates tariff exposure, reduces freight costs and inventory carrying costs, and increasingly benefits from automation investment tax credits that directly offset capital expenditure. For high-reliability programs in defense-adjacent, industrial, and automotive sectors where volume runs lower and quality requirements run higher, U.S. production often delivers a total landed cost within roughly 10 to 18 percent of China on many programs, while providing lead time, IP protection, and supply chain visibility that nearshore production cannot fully match. The cost-competitive case for domestic or nearshore production is closer than most OEMs assume.

The hidden costs that never appear in a China quote

Your China CM quote doesn’t include buffer stock requirements. With a 90 to 120 day effective replenishment cycle, transit plus customs plus inland freight plus safety stock, the working capital tied up in inventory is a real program cost that accrues every quarter. Intellectual property leakage risk, quality excursions caught late in a long supply chain, and currency and freight volatility don’t appear in the quote either. These aren’t hypothetical concerns: they are documented program costs that belong in any honest landed cost comparison.

The non-cost case: resilience factors that tip the reshoring decision

Lead time, inventory risk, and supply chain visibility

The operational reality of a China-sourced supply chain is a 90 to 120 day replenishment cycle when you account for ocean transit, port handling, customs clearance, and inland transport. A nearshore or domestic supply chain collapses that to 2 to 4 weeks. The working capital difference is substantial on its own. The ability to respond to a demand change, a component shortage, or a quality escape mid-cycle is a different category entirely. Supply chain resilience and reshoring go together precisely because resilience is a measurable reduction in program risk and inventory carrying cost, not just a strategic talking point.

IP risk, regulatory pressure, and customer-mandated domestic sourcing

Defense contractors and automotive OEMs are increasingly requiring country-of-origin documentation and domestic content percentages in their supply agreements. This isn’t a preference, it’s contractual compliance. Beyond customer mandates, IP leakage risk in Chinese manufacturing is a real and largely unquantified liability for companies with proprietary hardware designs. These pressures don’t appear in a landed cost model, but they represent material business risk. For programs where the landed cost differential is close, resilience and IP factors frequently tip the tariff-driven reshoring decision.

Federal incentives that change the 2026 reshoring calculus

The AMTC, CHIPS Act funding, and bonus depreciation

The Advanced Manufacturing Investment Credit (Section 48D) provides a 35 percent investment tax credit on qualified U.S. manufacturing equipment placed in service after December 31, 2025, per current IRS and Treasury guidance, verify the exact rate and eligibility rules against the relevant statute before modeling CAPEX. The One Big Beautiful Bill Act restored 100 percent bonus depreciation through 2029, allowing immediate expensing of CAPEX rather than stretching it across a multi-decade depreciation schedule. For a facility investing in production lines and automation, the combination of these two provisions dramatically changes the net cost of reshoring infrastructure. CHIPS Act grants and investment credits target semiconductor and electronics facilities specifically, including supply chain partners and component assemblers. For details on the Section 48D credit rules, review the latest regulatory guidance and summaries from authoritative sources.

The Section 48D deadline: why acting this year matters

The Section 48D Advanced Manufacturing Investment Credit is scheduled to expire on December 31, 2026. Construction must begin before January 1, 2027 to qualify. Companies that delay their reshoring evaluation past this year lose access to one of the most direct CAPEX offset tools in the current policy environment. This is a hard cutoff, and beginning the financial modeling and CAPEX planning now is the only way to capture it. Other incentives, including CHIPS Act funding and bonus depreciation, continue beyond 2026, but the Section 48D credit window does not.

State-level programs that stack with federal incentives

Property tax exemptions, workforce training grants, and site preparation incentives at the state level frequently complement federal programs. States with active semiconductor and electronics incentive programs, including Arizona (Arizona Commerce Authority), Texas (Texas Economic Development and Tourism), and New York (Empire State Development), can meaningfully reduce the net CAPEX cost of a reshoring decision when stacked with federal credits. The combined federal and state incentive picture makes reshoring CAPEX look substantially different from what a raw capital cost comparison would suggest.

A practical framework for making the reshoring decision

How tariffs affect the decision to reshore electronics production from China: a three-axis assessment

Structure the reshoring evaluation around three questions in parallel. First: what is your current tariff exposure by product line, and what does a revised landed cost model show for alternate geographies? Second: what is the operational and business risk of your current supply chain structure beyond the unit cost? Third: what CAPEX offsets are available if you commit to a reshoring transition this year? Running all three simultaneously prevents OEMs from making a cost-only decision that ignores strategic risk or available financial support, because each axis can independently change the outcome.

Scenario analysis and supplier mapping as the starting point

Before committing to a transition, the practical first step is scenario analysis across two or three alternative sourcing locations. Map your top-spend components, run the landed cost model by location using current tariff rates, and identify which programs cross the threshold where reshoring saves money and which are close enough to warrant further supplier qualification. This narrows scope quickly and turns a complex strategic question into a prioritized list of programs with clear economics attached.

How North American contract manufacturers support the transition

North American contract manufacturers with onshoring transition infrastructure, tariff-mitigating Approved Vendor List strategies, and programs built specifically for supply chain volatility are structured to support OEMs moving through this evaluation. Amtech works with OEMs at each stage of this process, from alternate component sourcing on existing programs to phased domestic production as volumes and qualifications align. The shift doesn’t have to be a lift-and-shift: it can be a structured migration that reduces tariff exposure incrementally while building toward a fully reshored supply chain on a timeline that works for your program.

The decision you’re already making by waiting

Tariffs have already changed the landed cost equation for most electronics categories. The cost models built before 2025 are wrong, in many cases understating total landed cost by 30 to 50 percent. Waiting for the trade environment to stabilize before running the analysis is itself a business decision, and it’s costing you the gap between what you’re currently paying and what a revised sourcing strategy would deliver.

Here’s where to start. Run your landed cost model with current tariff rates applied at the component line-item level. Evaluate the non-cost resilience factors, lead time, IP exposure, and customer-mandated domestic content requirements, alongside the unit economics. Then capture the 2026 incentives before the Section 48D credit expires at year-end; that specific window closes December 31, 2026 and does not reopen.

Understanding how tariffs affect the decision to reshore electronics production from China starts with an honest landed cost audit, and that’s exactly where Amtech begins. Whether you need a component-level tariff exposure analysis, a supplier mapping exercise, or a phased plan for moving production into North America, Amtech supports OEMs at each of those stages. The math has already changed. The question is whether your sourcing strategy has caught up.